- by Ahmed Shareek

Insuring a Sapphire Ring — Appraisals, Riders, and What Your Policy Actually Covers

- by Ahmed Shareek

For ring care alongside insurance: How to Care for a Sapphire Ring. For stone documentation: How to Read a GIA Sapphire Report. For the buying foundation: Ultimate Sapphire Buying Guide.

Most buyers spend considerable time and care choosing a sapphire engagement ring and almost no time thinking about what happens if it is lost, stolen, or damaged. Insurance is not a glamorous subject, but for a ring that represents a meaningful investment — typically $1,000 to $15,000 and sometimes much more — it is one of the most financially important decisions you make after the purchase.

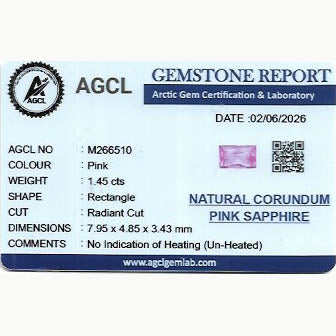

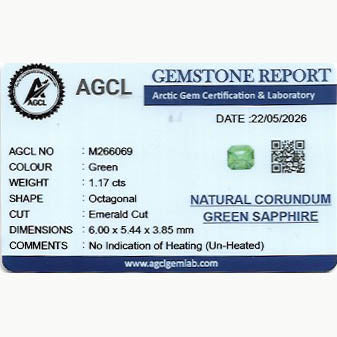

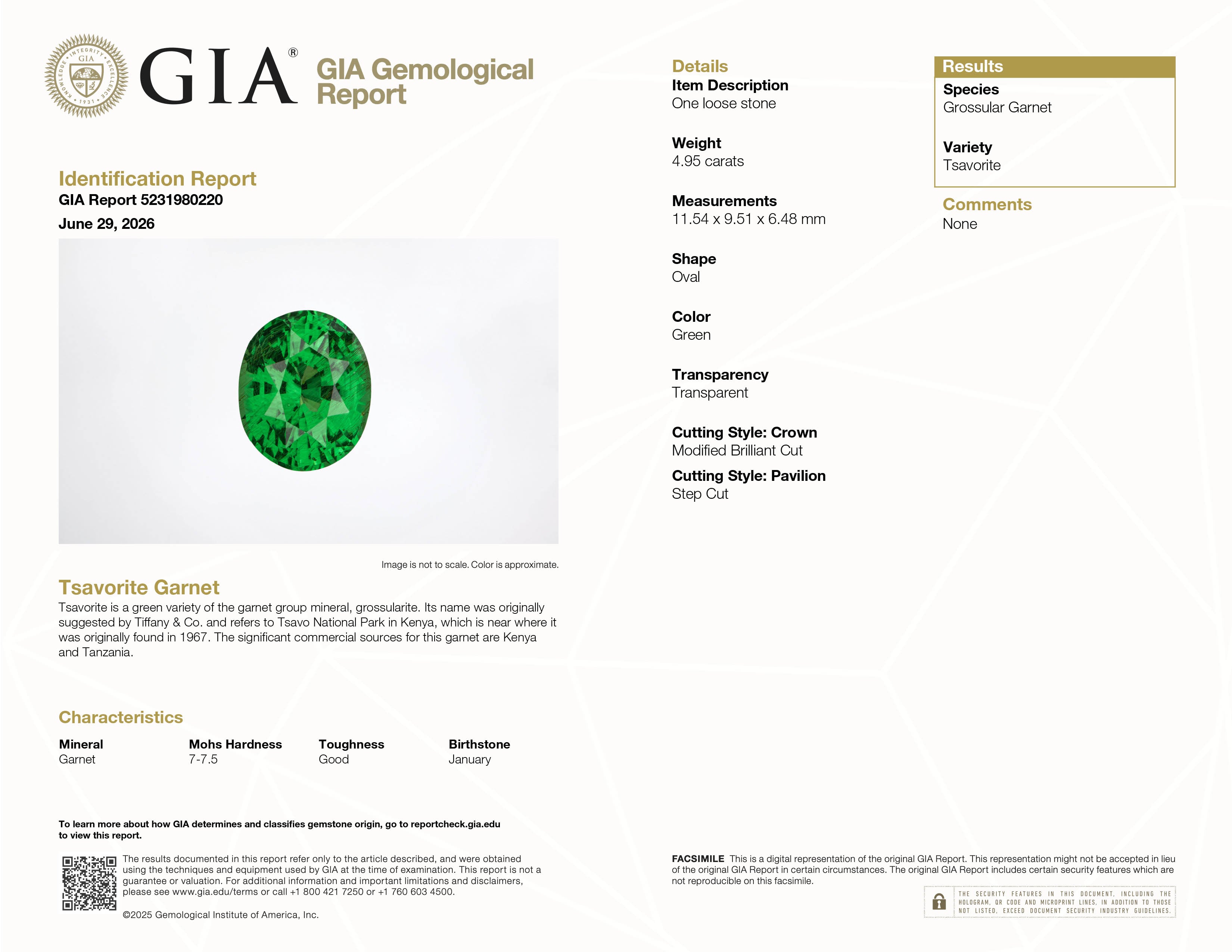

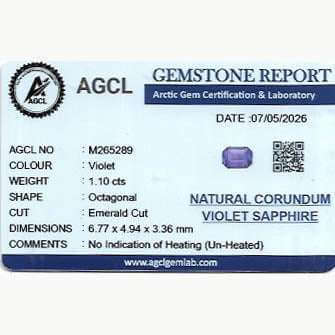

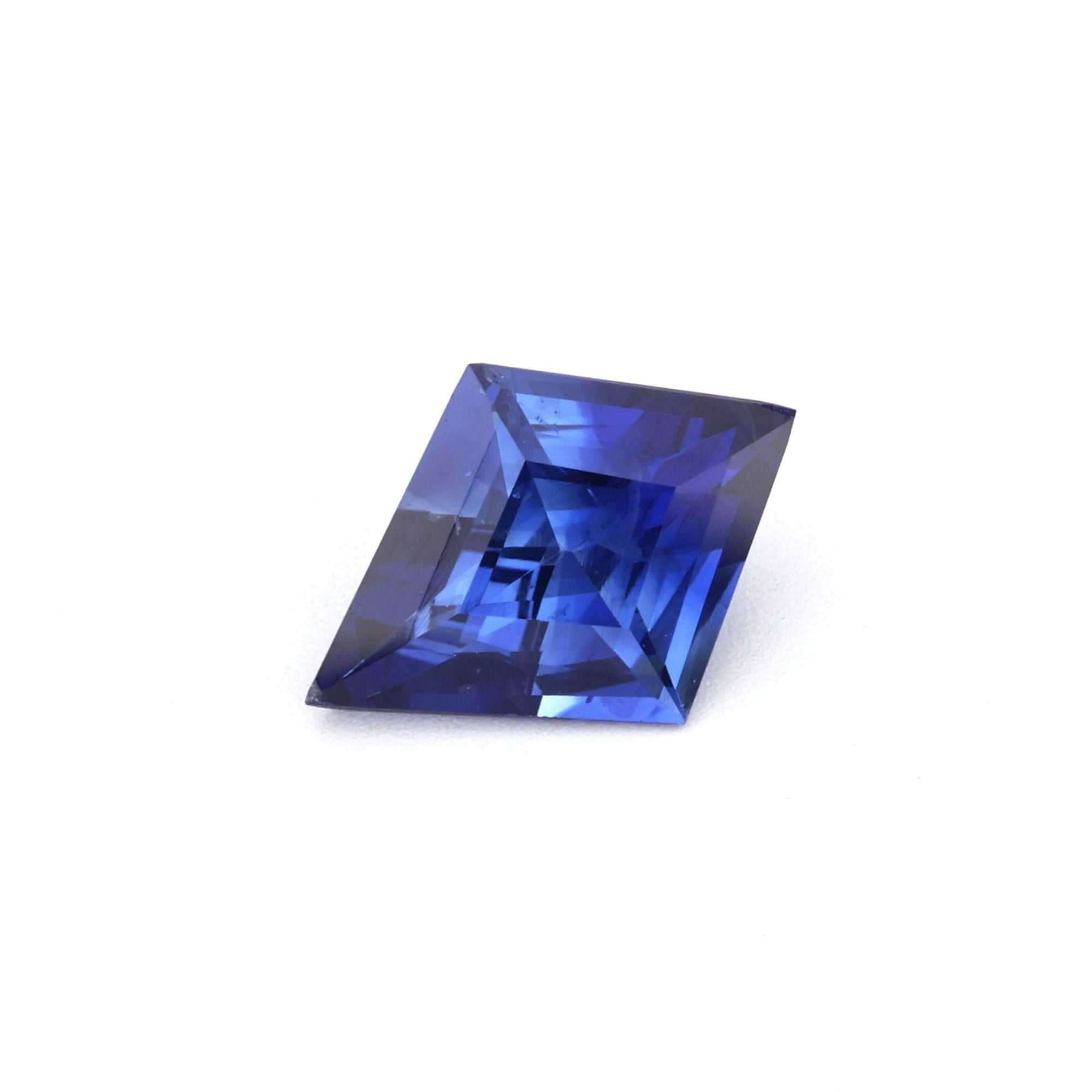

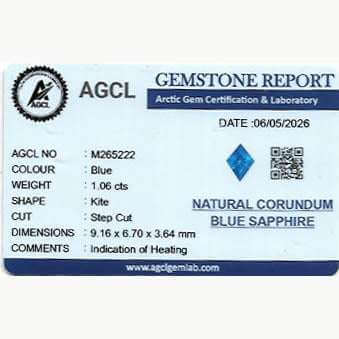

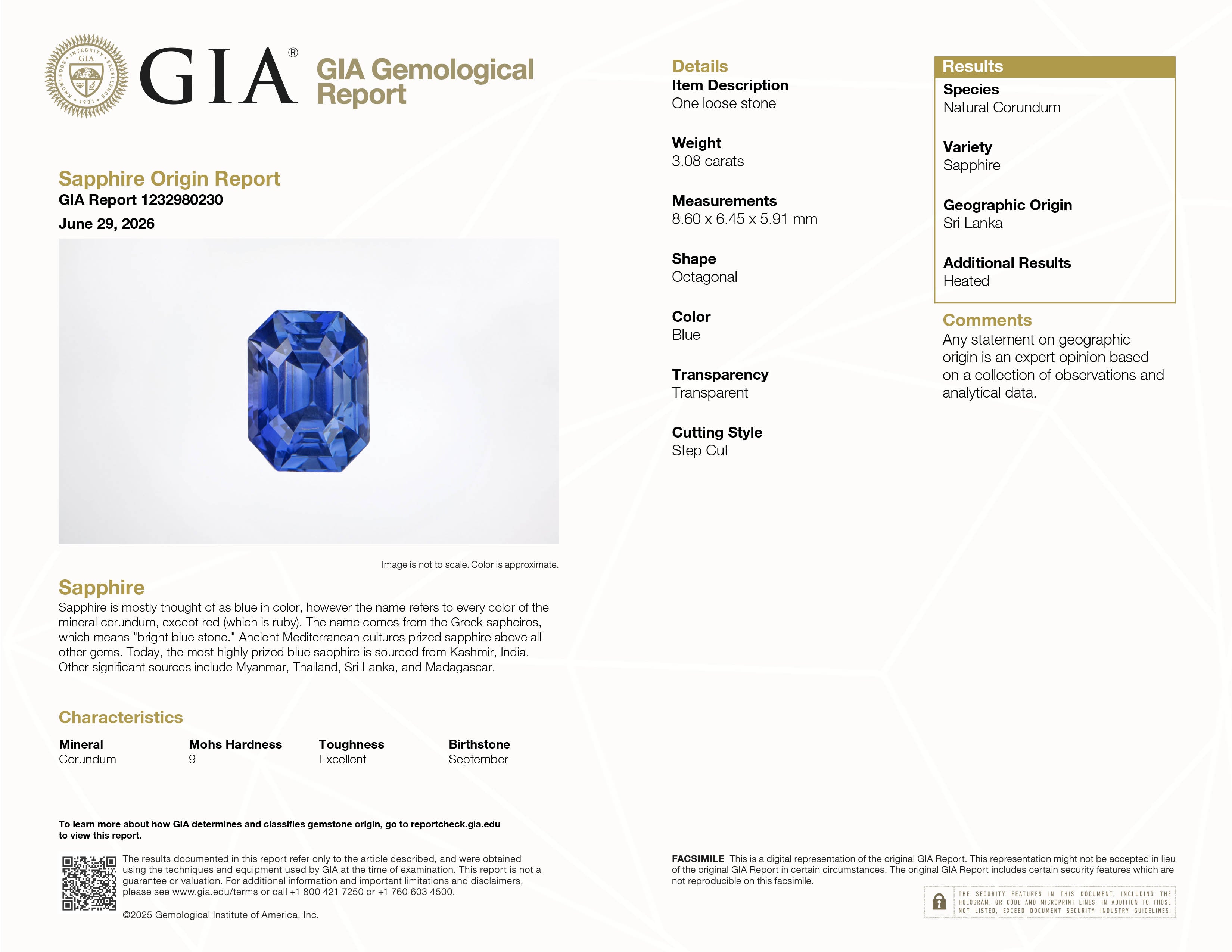

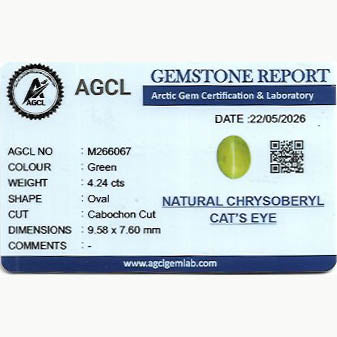

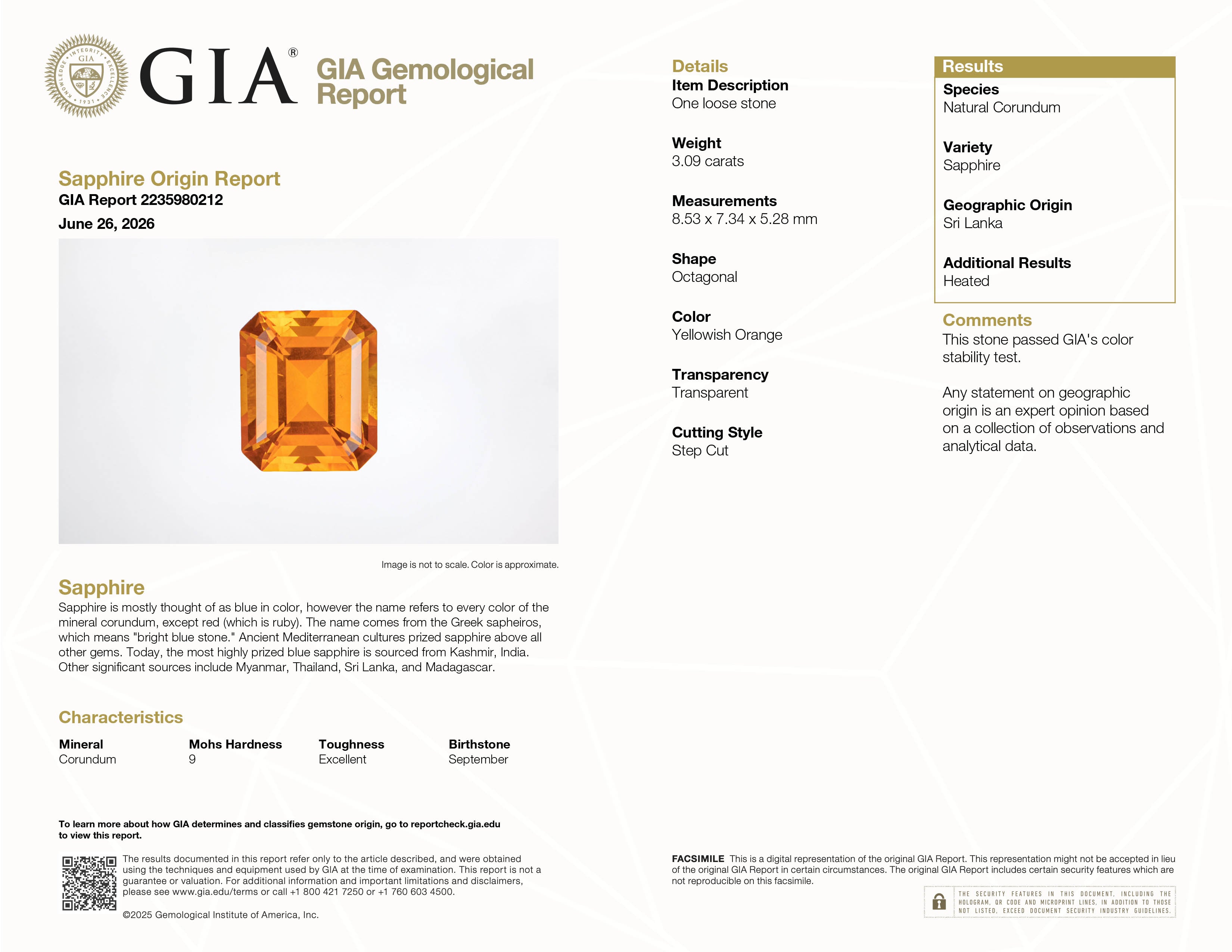

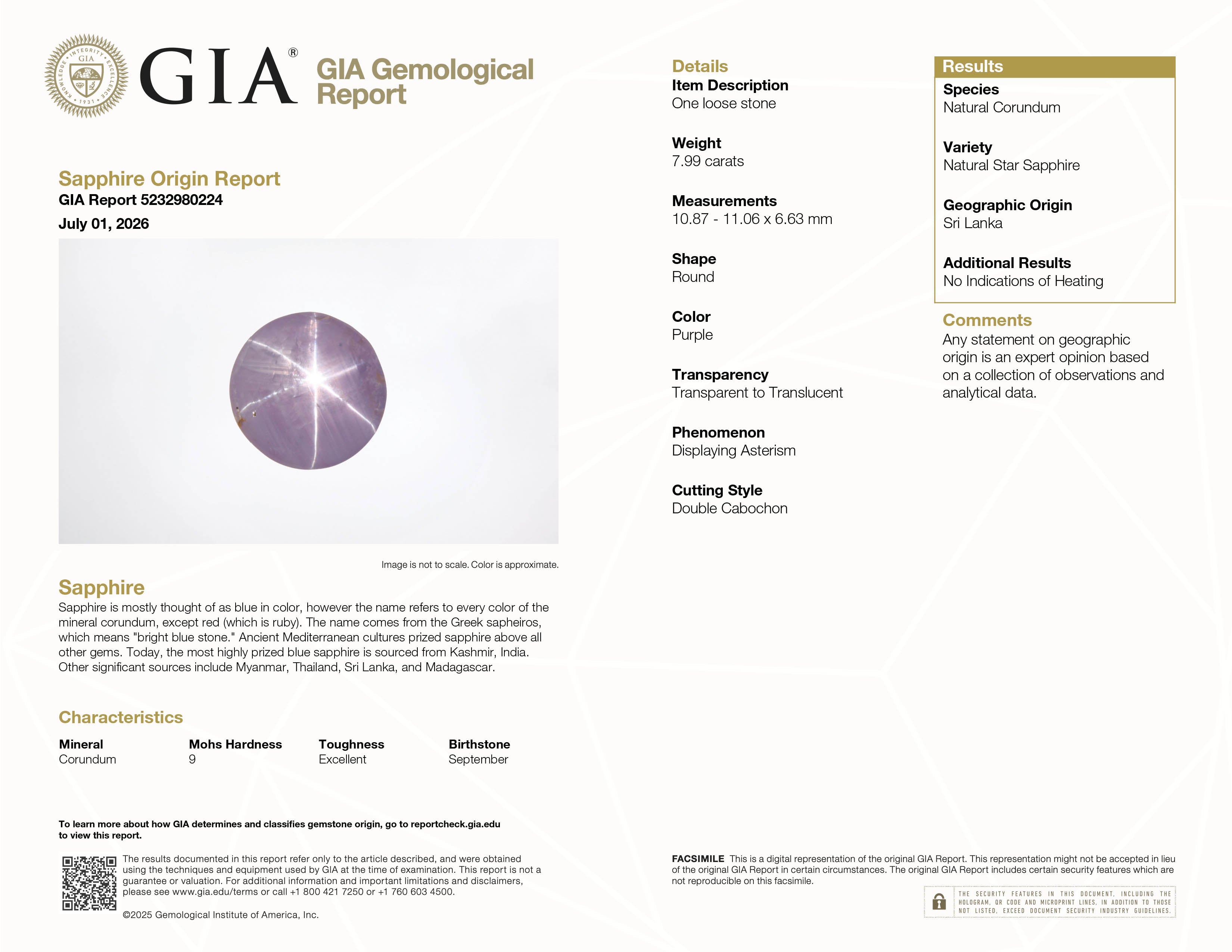

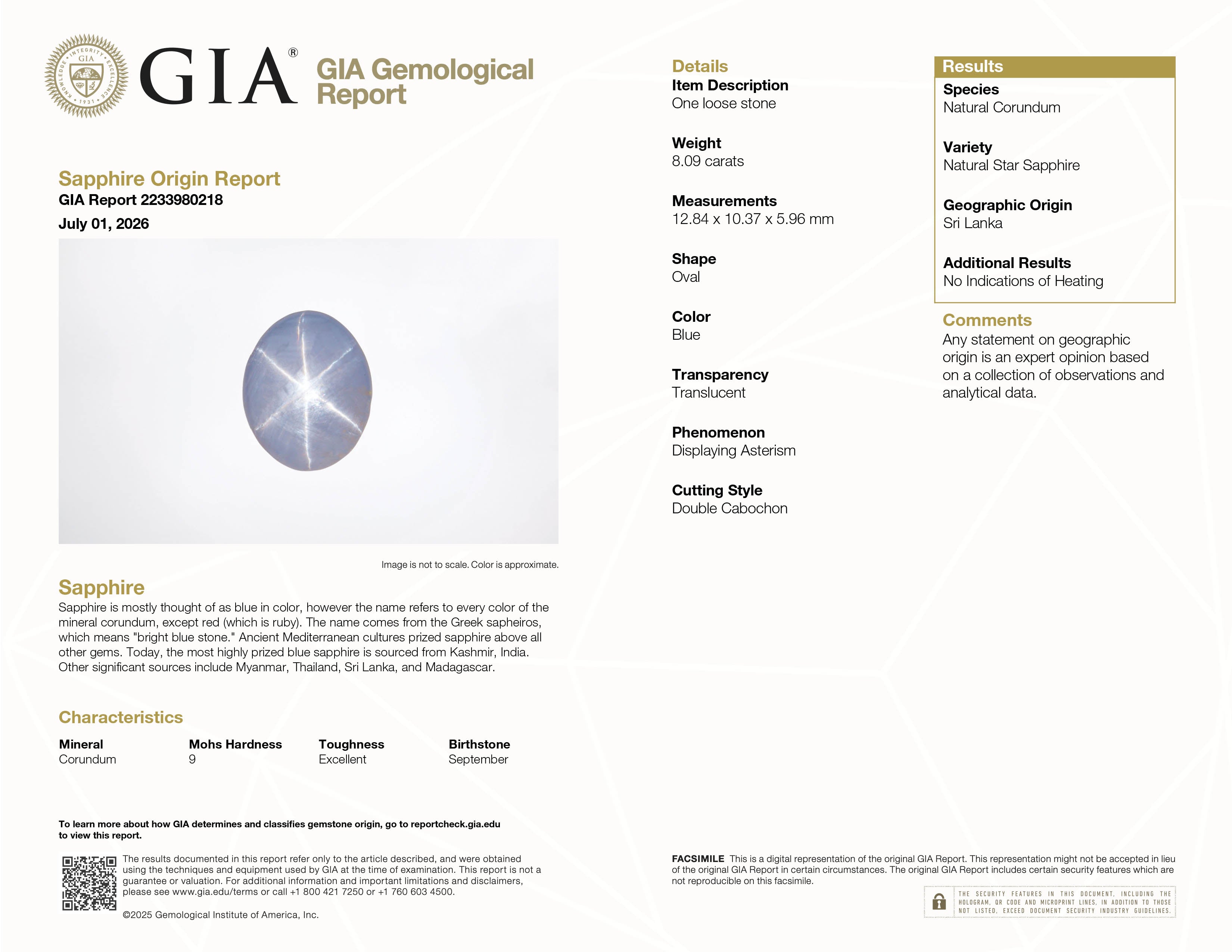

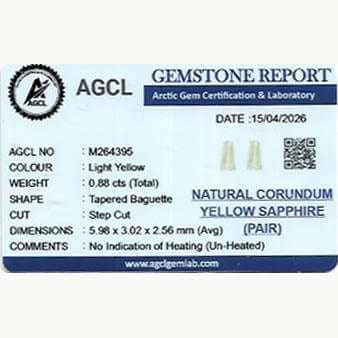

A proper insurance appraisal should include: a detailed description of the center stone (species, carat weight, measurements, color, clarity, treatment status from the laboratory report); a detailed description of the setting (metal type and karat, setting style, accent stones); reference to any existing laboratory report by report number; photographs; the appraiser's stated retail replacement value; and the appraiser's credentials, signature, and date.

Who should appraise it: Use a credentialed, independent appraiser with GIA Graduate Gemologist (GG) and American Society of Jewelry Appraisers (ASJA) or American Gem Society (AGS) membership. Avoid using the jeweler who sold you the ring. Independent appraisers typically charge $50-$150 per hour or $50-$200 per item.

Retail replacement value: Insurance appraisals typically state a retail replacement value — often higher than what you paid if you bought from a direct-source dealer like Crescent Gems. Do not ask the appraiser to lower the value to match what you paid. Update your appraisal every three to five years or sooner if sapphire prices have moved significantly.

Homeowner's or Renter's Insurance — Scheduled Item Rider: Standard homeowner's and renter's insurance typically includes only $1,000-$2,500 total jewelry coverage. A scheduled jewelry rider lists each item individually with its appraised value. Costs typically 1-2% of appraised value annually. May carry a deductible. Verify whether mysterious disappearance is covered and whether it's replacement value or actual cash value.

Standalone Jewelry Insurance: Dedicated jewelry insurance companies (Jewelers Mutual, GemShield, Lavalier) specialize exclusively in fine jewelry. Key features: agreed value coverage; worldwide coverage; mysterious disappearance coverage; no deductible options. Annual premium typically 1-2% of appraised value.

Theft: covered. Loss (mysterious disappearance): covered by dedicated jewelry insurers — this is the most important coverage term for rings, since most ring loss is unexplained. Accidental damage: covered. Normal wear and gradual deterioration: not covered. Intentional damage: not covered. The phrase “mysterious disappearance” on your policy is critical — verify it is explicitly included.

Replacement value (agreed value): The policy pays the full appraised value to replace the item with an equivalent piece, regardless of depreciation. This is what you want for fine jewelry. Actual cash value (ACV): The policy pays what the item is worth at the time of the claim, adjusted for depreciation. For fine sapphire jewelry, ACV is problematic because gemstone values do not necessarily depreciate — they can appreciate. Always verify your policy specifies replacement value, not ACV.

Keep: the GIA or laboratory report for the center stone (see our GIA report guide); the insurance appraisal; the purchase receipt or invoice; photographs from multiple angles; video. Store all documentation somewhere other than your home — a password-protected cloud folder works well. If the ring contains an unheated sapphire, explicitly draw your appraiser's attention to the GIA report's unheated designation so they factor in the unheated premium, not generic heated market rates.

Have your ring inspected professionally annually to check prong tightness, setting integrity, and any signs of wear. Prompt repair of damage prevents further loss. Keep appraisals updated. See our Sapphire Ring Care Guide for the full maintenance framework.

Report theft to police immediately. Contact your insurer promptly. Gather your documentation. Understand your replacement options — most dedicated jewelry insurance policies offer cash payment at the appraised value, or in-kind replacement through a jeweler of your choice. For damaged rings, get a repair estimate from a qualified jeweler before accepting any settlement.

Expect to pay 1-2% of the appraised value per year for a dedicated jewelry insurance policy with replacement value coverage and no deductible. For a ring appraised at $5,000: $50-$100/year. For a ring appraised at $15,000: $150-$300/year. For context on ring and stone values, see our what a good 1 carat costs and what a good 2 carat costs guides.

Questions about your specific stone's value or documentation? Email crescentgems@gmail.com — we respond within one business day.

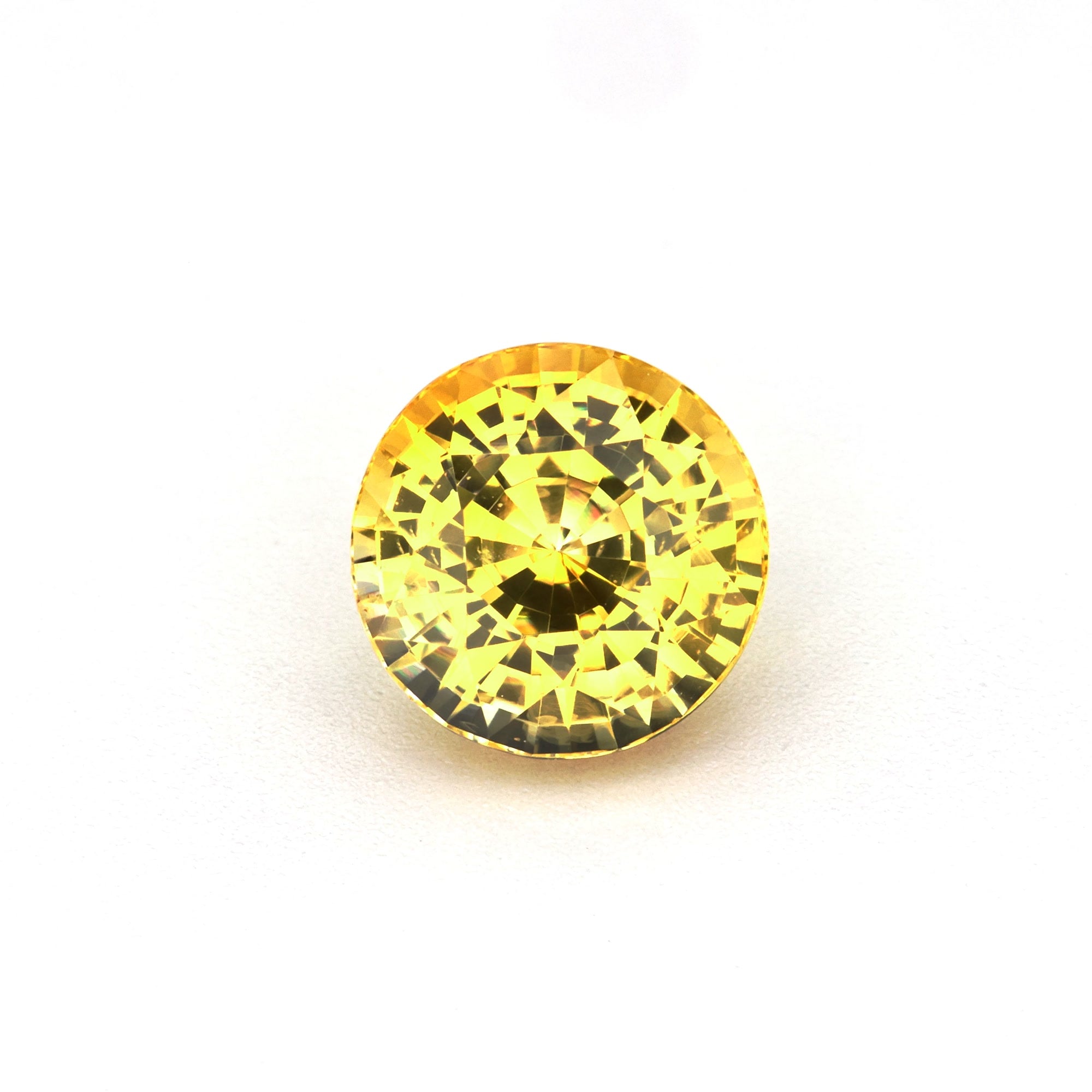

CG8451

1.50 ct Natural Heated Yellow Sapphire – Step-Cut Round

CG8448

CG8449

CG8447

CG8446

CG8444

CG8443

CG8442

CG8445

CG8433

The Ultimate Guide to Buying Natural Loose Sapphires

The definitive guide to buying a natural loose sapphire: colour, origin, treatment, cut, shape, certification, pricing, and engagement rings, with links to every Crescent Gems guide and collection.

Read moreabout The Ultimate Guide to Buying Natural Loose Sapphires

Custom Sapphire Rings — The Complete Guide to Designing Your Own

Read moreabout Custom Sapphire Rings — The Complete Guide to Designing Your Own

Cost of a 2 Carat Sapphire — Pricing, Scarcity, What Your Budget Buys

Read moreabout Cost of a 2 Carat Sapphire — Pricing, Scarcity, What Your Budget Buys

Cost of 1 carat Sapphire — Honest Pricing

Share: